And the slowest growing Member State this year is…

Economy 1 June 2015Clue: apparently its President in 2011 asked Greece to put up the Parthenon as collateral for the loan the country received from the EFSF. Yes, exactly, we are talking about Finland: the slowest growing country in the Euro area in 2015 according to the latest projections of the European Commission (excluding Cyprus which is forecasted still in recession).

The lost competitiveness

The Finnish economy has been stuck in recession for many years. Somehow it did not get much media attention but real GDP growth has been negative for the past three years and for 2015 the Commission expects a meagre 0.3% GDP growth. Simultaneously the unemployment rate has increased to almost 9% since 2008 when it was about 6%.

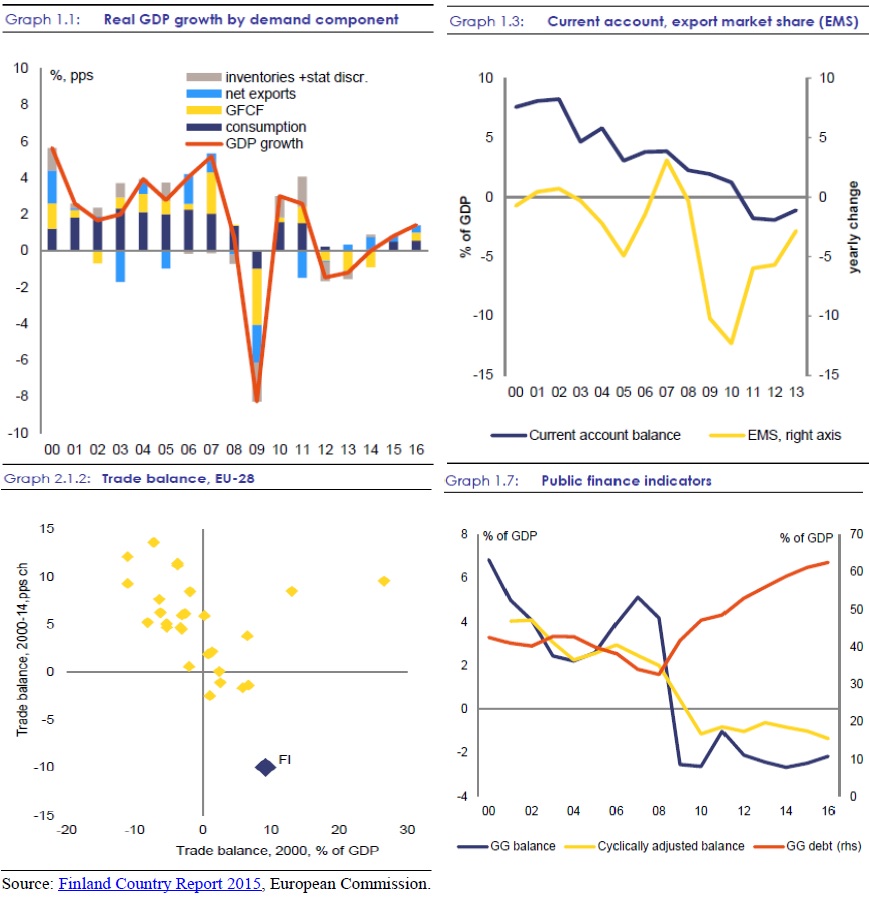

The story of Finland’s decline is not dissimilar to that of many other Eurozone countries. Faced with a sharp drop in demand in 2008 that, as shown in Graph 1.1, affected both the external and the internal sides, the Finnish Government initially responded with a fiscal expansion, evident from the blue line of Graph 1.7. However the expansion was followed by a fiscal retrenchment in 2010/2011. The move has plunged the country in a so-called double-dip recession from 2011 onwards that has lasted until last year (assuming of course that this year’s growth predictions are correct).

The most striking feature of the post-2008 situation is the sharp deterioration of Finland’s international competitiveness. This is well depicted by Graphs 1.3 and 2.1.2. The historically high current account surplus – that in 2000 was among the highest in the EU – turned into a deficit in 2010. At the same time, Finland kept on losing export market shares. The extent of the loss of competitiveness is such that the Commission estimates that Finland experienced the largest cumulative deterioration of the current account in the EU over the period 2000-2014.

It’s the rebalancing, stupid!

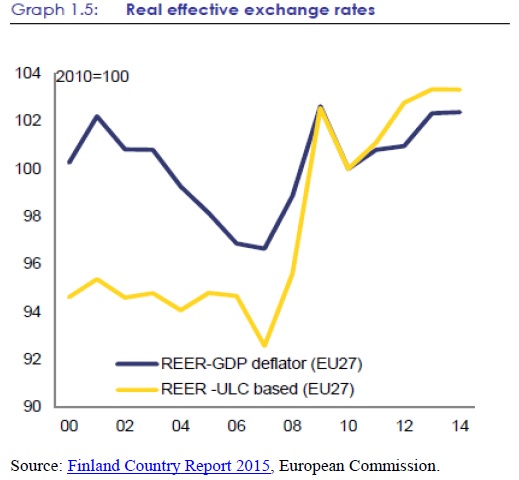

The deterioration of the current account in Finland is of course linked to the developments of its main trading partners. The depressed demand condition in most of its trading partners within the Euro area has meant a decline in export for Finnish goods and services. However, as the Commission notes, the shock experienced by the country’s export sector was not followed by a corresponding wage “adjustment”, meaning salaries did not decrease as output fell and actually with respect to export prices salaries even increased. This in turn has pushed up the Unit Labour Costs of Finland, compared to those of its neighbours. The result, as can be seen in Graph 1.5, has been an appreciation of the real exchange rate vis-à-vis the other EU countries.

As we have mentioned many times before in this newsletter (ie. here and here) in the absence of currency adjustments within the Eurozone, the relative competitiveness of countries depends on inflation differentials. This means that when wages, costs and prices in one Member State of the Eurozone increase more than in another, the country will experience an appreciation of the real exchange rate which translates into a loss of competitiveness, ie. lower exports and higher imports.

The crucial point with regards to Finland is that such loss of competitiveness vis-à-vis its partners of the Euro zone was not only to be expected but it is also absolutely necessary. This is, as a matter of fact, the essence of the so-called rebalancing within the Euro area.

Let us be a bit clearer on this. Up until 2008 some countries in the Euro area (Spain, Ireland, Greece, Portugal, etc.) accumulated current account deficit, hence they were losing competitiveness, vis-à-vis some other countries of the Euro area (Germany, Finland, the Netherlands, Austria, etc) which instead accumulated current account surpluses. Put it differently, the “deficit” countries were growing on the back of domestic demand, through their non-tradable sectors (like constructions); the surplus countries were instead growing out of external demand, through their tradable sectors (like machinery or automotive).

After 2008 the “deficit” countries found it increasingly difficult to finance their imports and to validate the external debt they had contracted over the years. In the absence of autonomous fiscal and monetary policies, all they could do was cutting spending, hence reducing imports. And so they did. This was done through what is commonly known as “austerity”. At the same time, these countries attempted to “rebalance” their economies. This means that they have been trying to prop up their tradable sectors and grow out of external demand since their domestic demand was compressed by the austerity policies. But to export more a country needs to become relatively more competitive than its partners. For this reason “deficit” countries pursued the so-called internal devaluation, reducing wages and costs.

For the strategy to be successful however it is not sufficient to simply reduce wages and costs because competitiveness is a relative phenomenon, so a country can only become more competitive if the others become less so. In other words, if Spain reduces its wages but Germany does the same, Spain is not becoming more competitive than Germany. If the objective of Spain is to become more competitive it is not the level of its wages that should be of concern but their dynamic vis-à-vis that of its trading partners.

Now back to Finland. Consider what would have happened to the country if it had kept its own currency. In the face of high current account surpluses – as it was the case before the crisis – its currency would have appreciated relative to that of its trading partners. This would have made the Finnish export sector increasing uncompetitive and at the same time would have increased the purchasing power of the Finnish citizens thus increasing their demand for imports. This would have effectively rebalanced the Finnish economy, which would have depended less and less on external demand for its growth and more on domestic demand. Simultaneously it would have made Finland’s trading partners more competitive as their weaker currency would have spurred export growth and depressed imports. Thus even Finland’s trading partners would have rebalanced, relying more and more on export and less and less on domestic demand.

In the absence of such currency adjustment, the rebalancing within the Euro zone has to be done through relative changes in wages and prices among countries. But unlike currency fluctuations, wages fluctuations are much more difficult to obtain. In fact, while countries like Spain or Greece have actively intervened to reduce their wages, the other side of the bargain was not implemented: Germany or the Netherlands did not increase their wages. This has prevented any meaningful rebalancing within the Eurozone from taking place.

In Finland however it seems that some sort of rebalancing actually took place. As its salaries kept increasing and its current account moved into deficit, the country became indeed less competitive than its trading partners in the Eurozone. In other words, the lost competitiveness of Finland is actually a necessary element of the currency union without which the cohabitation of different Member States within the Euro would become unsustainable.

We can’t all be competitive at the same time

Predictably however the loss of competitiveness of Finland has become a topic of electoral campaign and politicians of all sides promised to do more to re-launch the exports of the country. The new governing coalition is now in the making but it looks clear that the country intends to pursue a path of austerity and “pro-business” reforms, which means that they will try to reduce further their imports and expand their exports. Exactly the opposite of what a true Eurozone rebalancing would require from Finland, that is an expansion of domestic demand through an increase in wages and public and private investments.

But Finnish politicians should not be singled out for failing to appreciate the need to coordinate economic policies within the Eurozone. After seven years of crisis and more than 15 years of currency union, very few policy makers seem to have understood the rules of the game. The Euro zone remains stagnant and many countries are still stuck in a depression precisely because the rebalancing among Member States has not taken place.

Economic coordination in a currency area means that countries cannot be all competitive at the same time. If some Member States need to become more competitive and boost their exports, others need to accept to become less so and boost domestic demand instead. Otherwise it is not coordination, it is a race. A race to the bottom.

austerity competitiveness deficit economic growth Eurozone exports Finland recession trade unemployment wage cuts