Germany’s turn?

Economy 4 November 2014Clouds have gathered over the German economy in the last few months. Statistics show a GDP contraction in the third quarter of this year which led analysts to believe that the country may be entering a recession. Should we then conclude that even the German locomotive is coming to a halt in the crisis battered Eurozone?

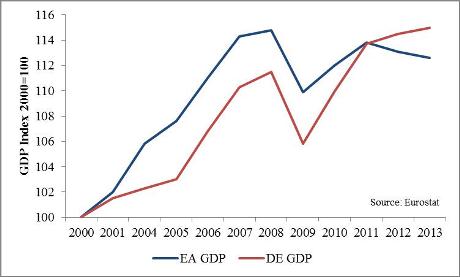

Well, one may claim that Germany was not the European locomotive in the first place. GDP growth in Germany has been subdued for the entire pre-crisis period. The rest of the Euro area grew at a much faster pace and only after the crisis the trend has reversed .

Well, one may claim that Germany was not the European locomotive in the first place. GDP growth in Germany has been subdued for the entire pre-crisis period. The rest of the Euro area grew at a much faster pace and only after the crisis the trend has reversed .

Germany’s performance over the past 15 years has been determined by external demand.

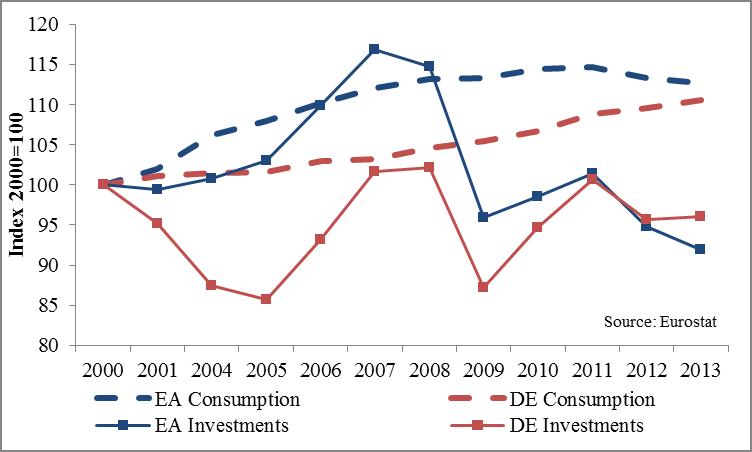

The country accumulated a growing trade surplus: from 2.7% of GDP in 2001-2005 to over 6% in 2013. At the same time its domestic demand has been much weaker (it actually had a negative growth rate between 2001 and 2005).

The difference in domestic consumption and investment compared to the Euro Area is striking. In the early 2000s the trends were evolving in opposite direction.

The main reason be hind falling consumption has been the very slow real wages growth (the slowest in the EU between 2000 and 2008) which was even negative between 2001 and 2005.

hind falling consumption has been the very slow real wages growth (the slowest in the EU between 2000 and 2008) which was even negative between 2001 and 2005.

Consequently the share of annual output going to labour decreased by almost 8 percentage points between 2000 and 2007 (by comparison: between the mid-70s and 2000 it had decreased by only 2 points).

Similarly, investments’ performance in Germany has been substantially below those of the rest of the EA, to the extent that the German press worries about the consequences of such process. In parallel to domestic demand contraction, Germany expanded its Net International Investment Position (NIIP). German financial institutions increasingly extended lines of credit to foreigners (mostly – but not only – within the EU).

The growth of NIIP has been massive: from 3% of Germany’s GDP in 2000 to 42% in 2012. The expansion of the NIIP is the financial counterpart of the Germany’s trade surplus: when a country buys German goods or services it also increases its indebtedness towards Germany.

In conclusion, Germany has been more like a sponge than a locomotive for the Eurozone. It has absorbed a growing share of other Member States’ demand by expanding its exports and credit. At the same time its demand stagnated, thereby also limiting imports from its trading partners. The potential of such strategy may therefore have hit its limits, since it rests on the possibility for foreign countries to cumulate debt.

For a change of strategy, Germany would not only need a change of mentality in its political class but also a structural reform of its national income distribution to stimulate consumption and investments. This would benefit also the rest of the Eurozone as it will increase Germans’ imports. Whether this will happen is largely for the German people to decide; the repercussions are however to be felt across the whole EU.

Related Articles

-

Prospects for EU’s economy in 2022

12 December 2021

An EU German post-electoral dilemma

4 October 2021

A missing migration agenda after the German elections

4 October 2021